Calculation of weighted moments and

cumulants of probability distributions and samples

[this page | pdf | references]

Equally-weighted statistics

The aggregate characteristics of probability distributions

and data samples are commonly analysed using a small number of statistics

corresponding to their first few moments, namely:

(a) The mean of the

distribution/sample,  , see MnMean, where:

, see MnMean, where:

(b) The ‘sample’ and the

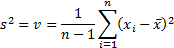

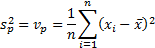

‘population’ variance,  and

and  respectively and

the corresponding ‘sample’ and ‘population’ standard deviation,

respectively and

the corresponding ‘sample’ and ‘population’ standard deviation,  and

and

of the

distribution/sample, see MnVariance,

MnPopulationVariance,

MnStdev and MnPopulationStdev,

where:

of the

distribution/sample, see MnVariance,

MnPopulationVariance,

MnStdev and MnPopulationStdev,

where:

In mathematical texts, is often referred

to as  and as

and as  .

.

(c) The skew (i.e.

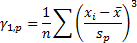

‘skewness’) of the distribution/sample,  , see MnSkew, where:

, see MnSkew, where:

(d) The kurtosis (or more

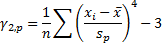

precisely the ‘excess’ kurtosis),  , of the

distribution/sample, see MnKurt,

where:

, of the

distribution/sample, see MnKurt,

where:

We see that the ‘sample’ variance differs from the

‘population’ variance by a factor of  representing the

loss of one degree of freedom when calculating the mean. This adjustment is

needed to ensure that the sample variance is an unbiased estimate of the

underlying population variance if the distribution is Normal, for finite sized

samples. In the large sample limit, i.e. where

representing the

loss of one degree of freedom when calculating the mean. This adjustment is

needed to ensure that the sample variance is an unbiased estimate of the

underlying population variance if the distribution is Normal, for finite sized

samples. In the large sample limit, i.e. where  ,

the two become equal.

,

the two become equal.

The formula for the skew and kurtosis given above are

properly ‘sample’ rather than ‘population’ measures. Both are dimensionless

quantities, and thus invariant to changes in the ‘scale’ of the distribution

(and its ‘location’) (i.e. if every element of the sample  was replaced by

was replaced by  , where

, where  (the

(the

representing a

change of scale, and the

representing a

change of scale, and the  representing a

change in location) then the skew and kurtosis would remain unaltered. We could

if we wished also define ‘population’ equivalents, see MnPopulationSkew, and

MnPopulationKurt,

where:

representing a

change in location) then the skew and kurtosis would remain unaltered. We could

if we wished also define ‘population’ equivalents, see MnPopulationSkew, and

MnPopulationKurt,

where:

Not equally-weighted

statistics

In some circumstances different elements of a sample should

be given different weights in the formulation of views regarding the overall

probability distribution. For example, there may be greater errors known to be

associated with some specific values used in constructing the sample, so less

credibility should be attached to them when deciding on the overall shape of

the distribution.

Given different weights,  to attach to each

data point (which might, for example, be associated with the square of the

standard error being ascribed to the relevant data point, say

to attach to each

data point (which might, for example, be associated with the square of the

standard error being ascribed to the relevant data point, say  ), derivation of

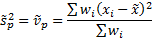

corresponding weighted ‘population’ statistics is relatively simple, e.g. the

weighted mean,

), derivation of

corresponding weighted ‘population’ statistics is relatively simple, e.g. the

weighted mean,  , the weighted

population variance,

, the weighted

population variance,  , the weighted

population standard deviation

, the weighted

population standard deviation  , the weighted

population skew,

, the weighted

population skew,  , and the weighted

population kurtosis,

, and the weighted

population kurtosis,  , see MnWeightedMean, MnWeightedPopulationVariance,

MnWeightedPopulationStdev,

MnWeightedPopulationSkew

and MnWeightedPopulationKurt,

may be defined as follows (dropping the explicit indexing of the summation

element to simplify the formulae):

, see MnWeightedMean, MnWeightedPopulationVariance,

MnWeightedPopulationStdev,

MnWeightedPopulationSkew

and MnWeightedPopulationKurt,

may be defined as follows (dropping the explicit indexing of the summation

element to simplify the formulae):

More difficult is to identify the correct way to incorporate

an appropriate small sample size adjustment to incorporate the right number of

degrees of freedom. Different commentators (or at least software providers

providing software downloadable from the Internet) appear to use different

approaches, particularly when deriving a suitable measure of weighted ‘sample’

skew.

The Nematrian website adopts the approach that small sample

size adjustment factors, at least for the simpler moments/cumulants, should

involve scale invariant factors that are reciprocals of expressions taking the

following form (for suitable combinations of  where

where

,

,  being

the ‘order’ of the relevant measure) which reproduce the equally-weighted

adjustment factors for cases where

being

the ‘order’ of the relevant measure) which reproduce the equally-weighted

adjustment factors for cases where  for

for  and

and

for

for  :

:

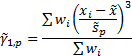

This implies that the most appropriate definitions of the weighted

sample variance,  , the weighted

sample standard deviation

, the weighted

sample standard deviation  and the weighted

sample skew,

and the weighted

sample skew,  , see MnWeightedVariance,

MnWeightedStdev and

MnWeightedSkew, are:

, see MnWeightedVariance,

MnWeightedStdev and

MnWeightedSkew, are:

where

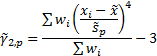

Using this methodology it is less clear exactly what small

sample size adjustment we should make when calculating a weighted (sample)

kurtosis measure, but see Rimoldini

(2013). In any case, some commentators such as Press et al.

(2007) suggest that kurtosis (and skew) “should be used with caution, or

better yet, not at all”. Kemp (2009)

also questions the appropriateness of using skew and kurtosis to identify how

non-Normal is a distributional form, see also TVaRForCubicQuantileQuantileRelationships.

The corresponding Cornish-Fisher

approximation that might otherwise be used to extrapolate the shape of the

distributional form seems in general to give inappropriate weight to the wrong

parts of the distributional form when assessing the extent of non-Normality.

Some software systems also allow users to calculate sample

‘moments’ relative to a predefined value, rather than the sample mean, but this

is not currently possible using existing pre-defined Nematrian web service

functions. It is not obvious to us whether it would be particularly useful in

practice. For example, Press et

al. (2007) note that using the formula defined above for the

(equally-weighted) sample skew has a standard error, if the sample is drawn

from a Normal distribution, of approximately  . However, if we replace

the in its definition

by the true mean of the distribution then its standard error rises to

approximately

. However, if we replace

the in its definition

by the true mean of the distribution then its standard error rises to

approximately  . The corresponding

approximate standard errors for kurtosis are

. The corresponding

approximate standard errors for kurtosis are  and

and  respectively. Thus

the computation of both skew and kurtosis becomes less accurate if we

use the true mean in their formulae! For ease of reference, the and formulae are

available directly using MnConfidenceLevelSkewApproxIfNormal

and MnConfidenceLevelKurtApproxIfNormal.

respectively. Thus

the computation of both skew and kurtosis becomes less accurate if we

use the true mean in their formulae! For ease of reference, the and formulae are

available directly using MnConfidenceLevelSkewApproxIfNormal

and MnConfidenceLevelKurtApproxIfNormal.

Weighted correlation correficients, weighted covariances and

weighted population covariances are defined in an equivalent manner, see MnWeightedCorrelations,

MnWeightedCovariances

and MnWeightedPopulationCovariances

respectively.