The t copula

[this page | pdf | back links]

The t copula is the copula that underlies the

multivariate Student’s t distribution.

|

Copula name

|

t copula

|

|

Common notation

|

|

|

Parameters

|

, a non-negative

definite , a non-negative

definite  matrix, i.e. a matrix that can

correspond to a correlation matrix matrix, i.e. a matrix that can

correspond to a correlation matrix

= degrees of

freedom ( = degrees of

freedom ( , usually is an integer

although in some situations a non-integral can arise) , usually is an integer

although in some situations a non-integral can arise)

(note in principle

each marginal distribution could in principle have a different number of

degrees of freedom although such a refinement is not commonly seen)

|

|

Domain

|

|

|

Copula

|

where  is

the inverse student’s

t function and is

the inverse student’s

t function and  is

the cumulative distribution function of the multivariate student’s t

distribution with arbitrary mean and matrix generator equal to is

the cumulative distribution function of the multivariate student’s t

distribution with arbitrary mean and matrix generator equal to

|

|

Kendall’s rank

correlation coefficient (for bivariate case),

|

Where  is the correlation coefficient

between the two variables is the correlation coefficient

between the two variables

|

|

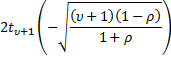

Coefficient of upper

tail dependence,

|

|

|

Coefficient of lower

tail dependence,

|

|

|

Other comments

|

If  (the

identity

matrix) then, in contrast to the Gaussian copula, we

do not recover the independence copula. (the

identity

matrix) then, in contrast to the Gaussian copula, we

do not recover the independence copula.

|

Nematrian web functions

Functions relating to the above distribution in the two-dimensional

case may be accessed via the Nematrian

web function library by using a DistributionName of “student’s t (2d)”.

For details of other supported probability distributions see here.

NAVIGATION LINKS

Contents | Prev