Integration of Piecewise Polynomials

against a Gaussian probability density function

[this page | pdf | references | back links]

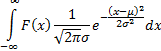

In a number of financial contexts it can be important to

calculate the following integral:

For example, this integral is relevant to calculating

moments of a fat-tailed distribution, i.e. one whose quantile-quantile plot

versus the Normal distribution,  ,

is not unity. The faster

,

is not unity. The faster  increases

as

increases

as  the

greater is the impact of fat-tailed behaviour, i.e. deviations from a density

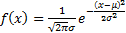

function of the form

the

greater is the impact of fat-tailed behaviour, i.e. deviations from a density

function of the form  .

Thus risk measures such as expected shortfall (effectively a first moment

computation, in which the leading element of is

of order

.

Thus risk measures such as expected shortfall (effectively a first moment

computation, in which the leading element of is

of order  )

are more sensitive to fat-tailed effects than Value-at-Risk risk measures

(effectively a zero moment computation, in which the leading element of is

of order

)

are more sensitive to fat-tailed effects than Value-at-Risk risk measures

(effectively a zero moment computation, in which the leading element of is

of order  ).

).

This integral can also appear in derivative pricing

analysis, if payoff is being approximated by a piecewise polynomial function

and the movement of the underlying is of a certain type (but see Valuing

polynomial payoffs in a Black Scholes World, which suggests that some

modification may be needed to cater for exponentials arising when converting

the partial differential equation arising under a Gauss-Weiner process to one

with ‘standard’ parabolic form).

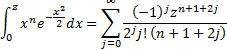

Hence, it becomes helpful to be able to calculate the

following integral rapidly:

If  is

large then we note that:

is

large then we note that:

Where

If is

small then for higher order coefficients the above computation runs into

machine rounding problems. It is then better to use a Taylor series expansion,

bearing in mind that:

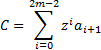

Hence (if  is

integral and

is

integral and  )

we have:

)

we have: