The generalised Pareto distribution

[this page | pdf | references | back links]

The generalised Pareto distribution (generalized Pareto

distribution) arises in Extreme Value Theory

(EVT). If the relevant regularity conditions are satisfied then the tail of a

distribution (above some suitably high threshold), i.e. the distribution of

‘threshold exceedances’, tends to a generalized Pareto distribution.

Care is needed with EVT because what we are in effect doing

with it is to extrapolate into the tail of the distribution. Extrapolation is

an intrinsically imprecise and subjective mathematical activity. We can in

effect view the regularity conditions that need to be satisfied if EVT applies

as corresponding to requiring that this extrapolation is done in a particular

manner.

![[SmartChart]](I/GeneralisedParetoDistribution_files/image001.gif)

![[SmartChart]](I/GeneralisedParetoDistribution_files/image002.gif)

![[SmartChart]](I/GeneralisedParetoDistribution_files/image003.gif)

|

Distribution name

|

Generalised

Pareto distribution (GPD)

|

|

Common notation

|

|

|

Parameters

|

=

shape parameter =

shape parameter

=

location parameter =

location parameter

=

scale parameter ( =

scale parameter ( ) )

|

|

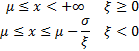

Domain

|

|

|

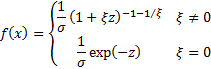

Probability density

function

|

where

|

|

Cumulative distribution

function

|

|

|

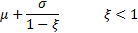

Mean

|

|

|

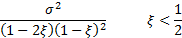

Variance

|

|

|

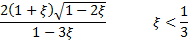

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Other comments

|

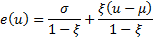

If  is uniformly

distributed, is uniformly

distributed,  then the

variable then the

variable  . .

The mean excess function for a GPD, i.e.  takes a

particularly simple form which is linear in ,

i.e. takes a

particularly simple form which is linear in ,

i.e.

|

Nematrian web functions

Functions relating to the above distribution may be accessed

via the Nematrian

web function library by using a DistributionName of “generalised

pareto”. For details of other supported probability distributions see here.

NAVIGATION LINKS

Contents | Prev | Next