Tail Value-at-Risk

[this page | pdf | references | back links]

The Tail Value-at-Risk, TVaR, of a portfolio  is

defined as the expected outcome (loss), conditional on the loss exceeding the Value-at-Risk (VaR), of

the distribution.

is

defined as the expected outcome (loss), conditional on the loss exceeding the Value-at-Risk (VaR), of

the distribution.

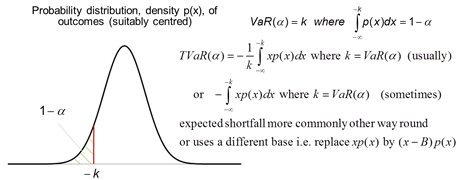

Where the support of the

distribution is continuous the VaR with confidence level  is usually

defined as follows:

is usually

defined as follows:

The corresponding Tail Value-at-Risk would then be defined

as:

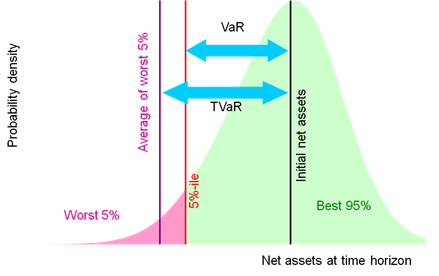

Visually the difference between VaR and Tail VaR may be

seen in either of the following charts:

VaR is not (in general) a coherent risk

measure, whilst TVaR is. VaR is arguably more shareholder focused and TVaR more

regulator/customer focused, see VaR versus TVaR mindsets.

Writers use Tail VaR (TVaR) and Conditional VaR

(CVaR) largely interchangeably, usually with the same loss trigger as the

quantile level that would otherwise be applicable if the focus was on VaR.

Occasionally, TVaR and/or CVaR are differentiated, with one being expressed in

terms of the loss beyond the VaR rather than below zero. However, such a

definition inherits some technical weaknesses attributable to VaR (i.e. that it

no longer exhibits diversification properties we might ‘expect’ a risk measure

to exhibit.

Another term that means much the same thing is Conditional

Tail Expectation (CTE), although perhaps this is more likely to refer to

the right tail of a distribution rather than the left tail, i.e. it might focus

on upside rather than downside, and the bound beyond which it is calculated may

not be expressed in a VaR-like form.

Expected

Shortfall has a similar meaning, but might use a trigger level set more

generically, e.g. it might include all returns below some level (e.g. zero) and

more commonly might no longer contain the  multiplier

included in the definition of TVaR a above.

multiplier

included in the definition of TVaR a above.

If several different risk exposures are contributing to the

overall TVaR then it often becomes important to identify the contribution each

is making to the total. This can be done using marginal Tail Value-at-Risk

(or marginal TVaR).