WeightedDesmooth_AR1

[this page | pdf | back links]

Function Description

Returns an array corresponding to the AR(1) weighted

de-smoothed (or ‘de-correlated’) values of a series, as described in the book Extreme Events. This

involves:

(a) Postulating

(for, say, a return series) that there is some underlying ‘true’ return series,

, and that the observed

series,

, and that the observed

series,  , derives from it via a

first order autoregressive model,

, derives from it via a

first order autoregressive model,  ;

;

(b) Identifying the value

of  (between 0 and 0.5) for

which has zero weighted first

order correlation (which implies that the weighted covariance between

(between 0 and 0.5) for

which has zero weighted first

order correlation (which implies that the weighted covariance between  and

and  is zero; and

is zero; and

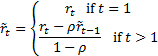

(c) Using this value

of deriving using the following

formula:

In step (b) we weight the elements in the covariance

computation using weights  (where

(where  corresponds to the

weight given to the component arising from the term in

corresponds to the

weight given to the component arising from the term in  .

.

The value of in (b) can be accessed

using MnWeightedDesmooth_AR1_rho.

If the weights are equal then returns the same as MnDesmooth_AR1.

NAVIGATION LINKS

Contents | Prev | Next

Links to:

-

Interactively run function

-

Interactive instructions

-

Example calculation

-

Output type / Parameter details

-

Illustrative spreadsheet

-

Other Statistical functions

-

Computation units used

Note: If you use any Nematrian web service either programmatically or interactively then you will be deemed to have agreed to the Nematrian website License Agreement