Desmooth_AR1_rho

[this page | pdf | back links]

Function Description

Returns the de-smoothing parameter corresponding to the

AR(1) de-smoothed (or ‘de-correlated) values of a series, as described in the

book Extreme Events.

This involves:

(a)

Postulating (for, say, a return series) that there is some underlying

‘true’ return series,  , and that the observed

series,

, and that the observed

series,  , derives from it via a

first order autoregressive model,

, derives from it via a

first order autoregressive model,  ; and

; and

(b) Identifying

the value of  (between 0 and 0.5) for

which has zero first order

correlation (which implies that the covariance between

(between 0 and 0.5) for

which has zero first order

correlation (which implies that the covariance between  and

and  is zero.

is zero.

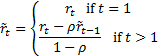

The de-smoothed series,  ,

can then be derived using the following formula, see MnDesmooth_AR1:

,

can then be derived using the following formula, see MnDesmooth_AR1:

NAVIGATION LINKS

Contents | Prev | Next

Links to:

-

Interactively run function

-

Interactive instructions

-

Example calculation

-

Output type / Parameter details

-

Illustrative spreadsheet

-

Other Statistical functions

-

Computation units used

Note: If you use any Nematrian web service either programmatically or interactively then you will be deemed to have agreed to the Nematrian website License Agreement