Extreme Events – Specimen Question

A.2.2(b) – Answer/Hints

[this page | pdf | references | back links]

Return

to Question

Q. Using a first order

autoregressive model, de-smooth the observed returns for Index B to derive a

return series that you think may provide a better measure of the underlying

behaviour of the relevant asset category.

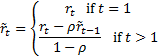

The approach for de-smoothing (or ‘de-correlating’) such

returns suggested in the book Extreme Events involves

assuming that there is some underlying ‘true’ return series,  , and that

the observed series,

, and that

the observed series,  , derives

from it via a first order autoregressive model,

, derives

from it via a first order autoregressive model,  . We will

assume that the autoregressive model actually applies to the logged returns,

which are given in ExtremeEventsQuestionsAndAnswers2_1a.

. We will

assume that the autoregressive model actually applies to the logged returns,

which are given in ExtremeEventsQuestionsAndAnswers2_1a.

If we assume that the corresponding are

independent, identically distributed (normal) random variables with standard

deviation  (and mean

0 given that we have standardised the data) then the (expected) variance of the

series

(and mean

0 given that we have standardised the data) then the (expected) variance of the

series  , will be

, will be  and the

(expected) covariance of the series

and the

(expected) covariance of the series  with the

series

with the

series  will be

will be  .

.

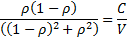

One way of proceeding would be to estimate  as

the solution to the equation:

as

the solution to the equation:

More precisely, since the above does not differentiate

between and  we

would probably choose the closest

to zero (and, ideally, we would expect it to be positive and smaller than 0.5,

which also requires

we

would probably choose the closest

to zero (and, ideally, we would expect it to be positive and smaller than 0.5,

which also requires  to be

positive, as a value of outside

this range would be implausible).

to be

positive, as a value of outside

this range would be implausible).

In this instance:

|

Statistic (using logged returns)

|

Value

|

|

(Sample*) Variance of (= ) )

|

0.008575828

|

|

(Sample*) Covariance of with (=)

|

0.002896449

|

|

Ratio (= ) )

|

0.337746

|

|

Estimated

|

0.279955

|

* Ideally, the Variance and Covariance should both include

the same small sample size adjustment, i.e. both be “sample” or both be

“population” estimates. The Microsoft Excel functions, VAR, VARP and COVAR, are

somewhat confusing in this respect, since COVAR is calculated using a

multiplier  , and is

therefore properly a “population” statistic and consistent with VARP, whilst

VAR is calculated using a multiplier of

, and is

therefore properly a “population” statistic and consistent with VARP, whilst

VAR is calculated using a multiplier of  , and so

is a “sample” statistic. The Nematrian website’s web functions are clearer as

it provides both a MnCovariance

function and a MnPopulationCovariance

function.

, and so

is a “sample” statistic. The Nematrian website’s web functions are clearer as

it provides both a MnCovariance

function and a MnPopulationCovariance

function.

Ignoring small sample size adjustments, estimates of can be

then be found using:

However, if we do this in practice we find that there are

second order effects that mean that estimating as above

still leaves some residual autocorrelation:

|

Period

|

(logged

returns of B)

|

(first

pass)

|

|

1

|

0.0487902

|

0.0487902

|

|

2

|

-0.1743534

|

-0.2611119

|

|

3

|

-0.1255632

|

-0.0728617

|

|

4

|

-0.0304592

|

-0.0139731

|

|

5

|

-0.0976128

|

-0.1301320

|

|

6

|

-0.0010005

|

0.0492060

|

|

7

|

-0.0801260

|

-0.1304104

|

|

8

|

0.0276152

|

0.0890558

|

|

9

|

0.1231022

|

0.1363395

|

|

10

|

0.0148886

|

-0.0323317

|

|

11

|

-0.1109316

|

-0.1414913

|

|

12

|

0.1106465

|

0.2086780

|

|

13

|

0.1646666

|

0.1475549

|

|

14

|

0.0925792

|

0.0712046

|

|

15

|

0.0797350

|

0.0830516

|

|

16

|

-0.0650720

|

-0.1226626

|

|

17

|

-0.0812101

|

-0.0650933

|

|

18

|

-0.0232686

|

-0.0070071

|

|

19

|

0.0525925

|

0.0757649

|

|

20

|

0.0276152

|

0.0088945

|

|

|

|

|

|

Variance (=)

|

0.0085758

|

0.0138041

|

|

Covariance (=)

|

0.0028964

|

0.0007054

|

|

Ratio (=)

|

0.3377457

|

0.0511003

|

|

Estimated

|

0.2799546

|

|

Better, therefore, is to use a root search algorithm in

which we explicitly search for the (ideally

between 0 and 0.5) for which has zero

autocorrelation. This can be done using the Nematrian MnDesmooth_AR1 or MnDesmooth_AR1_rho

functions (the former returns the desmoothed series, the latter returns the

value of for which

has zero

autocorrelation). Given the form of the problem given here, these provide the

following de-smoothed series (with rho equal to 0.31094682):

|

Period

|

(logged

returns of B)

|

(de-smoothed)

|

|

1

|

0.0487902

|

0.0487902

|

|

2

|

-0.1743534

|

-0.2750507

|

|

3

|

-0.1255632

|

-0.05810445

|

|

4

|

-0.0304592

|

-0.01798381

|

|

5

|

-0.0976128

|

-0.13354672

|

|

6

|

-0.0010005

|

0.05881321

|

|

7

|

-0.0801260

|

-0.14282465

|

|

8

|

0.0276152

|

0.10452905

|

|

9

|

0.1231022

|

0.13148365

|

|

10

|

0.0148886

|

-0.03772687

|

|

11

|

-0.1109316

|

-0.14396646

|

|

12

|

0.1106465

|

0.22554488

|

|

13

|

0.1646666

|

0.13719425

|

|

14

|

0.0925792

|

0.07244591

|

|

15

|

0.0797350

|

0.08302433

|

|

16

|

-0.0650720

|

-0.13190296

|

|

17

|

-0.0812101

|

-0.05833410

|

|

18

|

-0.0232686

|

-0.00744471

|

|

19

|

0.0525925

|

0.07968530

|

|

20

|

0.0276152

|

0.00411769

|

|

|

|

|

|

Variance (=)

|

0.0085758

|

0.01487681

|

|

Covariance (=)

|

0.0028964

|

0

|

|

Ratio (=)

|

0.3377457

|

0

|

Note:

(a) In

general de-smoothing increases the variance of the return series being

analysed. Here it has gone from 0.0926 to 0.1219.

(b) Whilst

the problem would usually be stated as shown, it perhaps makes more sense not

to make the arbitrary implicit assumption that the smoothing is around a mean

of zero, but around some mean (that is, for example, estimated from the data),

i.e. as if the model was  .

.

(c) We

might not necessarily want to give equal weight to each observation. This is

possible using the Nematrian MnWeightedDesmooth_AR1

and MnWeightedDesmooth_AR1_rho

functions.

NAVIGATION LINKS

Contents | Prev | Next | Question