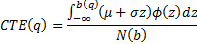

Identifying a formula for the (lower)

conditional tail expectation (CTE) of a normal distribution that does not

explicitly include integral signs but instead refers to the unit normal density

function and the unit normal cumulative distribution function

[this page | pdf | back links]

The (lower) conditional tail expectation (CTE) of a random

variable for a given cut-off,  , is

defined as the expected value of the random given that it is below the relevant

cut-off. It is thus very closely aligned with the Tail Value-at-Risk

(TVaR) of the distribution, since the TVaR is the CTE for a specific cut-off.

For a normal

distribution the CTE is thus:

, is

defined as the expected value of the random given that it is below the relevant

cut-off. It is thus very closely aligned with the Tail Value-at-Risk

(TVaR) of the distribution, since the TVaR is the CTE for a specific cut-off.

For a normal

distribution the CTE is thus:

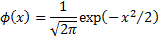

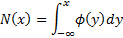

The unit normal distribution function,  , and

the unit Normal cumulative distribution function,

, and

the unit Normal cumulative distribution function,  , are

defined as follows:

, are

defined as follows:

Substituting  in the

above formula for the CTE we obtain, where

in the

above formula for the CTE we obtain, where  ):

):

We can re-express this in a form that relies only on and by

noting the following:

where  is

constant and furthermore as

is

constant and furthermore as  and

and  decays

sufficiently fast to zero as

decays

sufficiently fast to zero as  we have

we have

. Hence:

. Hence: