Enterprise Risk Management Formula Book

4. Statistical distributions

[this page | pdf | back links]

4.1 Probability distribution terminology

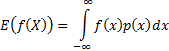

Suppose a (continuous) real valued random variable,  , has a probability density function

(or pdf)

, has a probability density function

(or pdf)  . Then

the probability of taking

a value between

. Then

the probability of taking

a value between  and

and  where

where  is

infinitesimal,

is

infinitesimal,  , is

, is  .

.

The expected value of a function  (given

this pdf) is defined (if the integral exists) as follows and is also sometimes

written

(given

this pdf) is defined (if the integral exists) as follows and is also sometimes

written  :

:

For to be a

pdf it must exhibit certain basic regularity conditions including  .

.

The mean,

variance, standard deviation, cumulative distribution

function (cdf or just distribution function), inverse cumulative

distribution function (inverse cdf or just inverse function

or quantile function), skewness (or skew),

(excess) kurtosis, mean

excess function,  ’th central

and non-central moments and entropy are defined as:

’th central

and non-central moments and entropy are defined as:

The cumulants (sometimes called semi-invariants),

, of a

distribution, if they exist, are defined via the cumulant generating function,

i.e. the power series expansion

, of a

distribution, if they exist, are defined via the cumulant generating function,

i.e. the power series expansion  of

of  . The

mean, standard deviation, skewness and (excess) kurtosis of a distribution are

. The

mean, standard deviation, skewness and (excess) kurtosis of a distribution are  ,

,  ,

,  and

and

The mode

of a (continuous) distribution, i.e.  , is the

value at which is

largest.

, is the

value at which is

largest.

The median,

upper quartile and lower quartile etc. (or more generally percentile) of a

(continuous) distribution are  ,

,  ,

,  etc. (or

etc. (or

) respectively.

) respectively.

Definitions of the above for discrete real-valued random

variables are similar as long as the integrals involved are replaced with sums

and the probability density function by the probability mass function

, i.e.

the probability of taking

the value

, i.e.

the probability of taking

the value  .

.

Some of the above are not well defined or are infinite for

some probability distributions.

If a discrete random variable can only take values which are

non-negative integers, i.e. from the set  then

the probability generating function is defined as:

then

the probability generating function is defined as:

Characteristic functions and (if they exist) central moments

and moment generating functions can nearly always be derived from non-central

moments by applying the binomial expansion, e.g.  ,

,  etc.

(where is a

constant)

etc.

(where is a

constant)

The domain (more fully, the domain of definition

or range) of a (continuous) probability distribution is the set of

values for which the probability density function is defined. The support

of a (discrete) probability distribution is the set of values of for

which  is

non-zero. The usual convention for a continuous function is to define the

distribution only where the probability density function would be non-zero and

for a discrete function (usually) to define the distribution only where the

probability mass function is non-zero, in which case the domain/range and

support coincide.

is

non-zero. The usual convention for a continuous function is to define the

distribution only where the probability density function would be non-zero and

for a discrete function (usually) to define the distribution only where the

probability mass function is non-zero, in which case the domain/range and

support coincide.

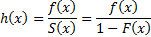

The survival function (or reliability function)

is the probability that the variable takes a value greater than (i.e.

probability a unit survives beyond time if is

measuring time) so is:

The hazard function

(also known as the failure rate) is the ratio of the pdf to the survival

function, so is:

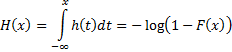

The cumulative hazard function is the integral of the

hazard function (i.e. the probability of failure at time given

survival to time , if is

measuring time) so is:

Definitions, characteristics and common interpretations of a

variety of (discrete and continuous) probability distributions are given in

Appendix A.

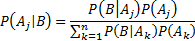

The probability that  occurs

given that occurs,

occurs

given that occurs,

is

defined for

is

defined for  as:

as:

For discrete random variables, , , the

expected value of  given

that occurs,

given

that occurs,

is

defined as follows, where

is

defined as follows, where  is the

range of :

is the

range of :

The following relationships apply:

If  is a

vector of (continuous) random variables then its (multivariate) pdf

is a

vector of (continuous) random variables then its (multivariate) pdf  and its

cdf

and its

cdf  satisfy:

satisfy:

The covariance between  and

and  is

is  and the

(Pearson) correlation coefficient is

and the

(Pearson) correlation coefficient is  . The

covariance matrix and the (Pearson) correlation matrix for multiple series are

the matrices

. The

covariance matrix and the (Pearson) correlation matrix for multiple series are

the matrices  and

and  which

have as their elements

which

have as their elements  and

and  respectively.

respectively.

4.2 Bayes theorem

Let  be a

collection of mutually exclusive and exhaustive events with probability of

event

be a

collection of mutually exclusive and exhaustive events with probability of

event  occurring

being

occurring

being  for

for  . Then,

for any event

. Then,

for any event  such

that

such

that  the

probability,

the

probability,  , of occurring

conditional on occurring

(more simply the probability of given )

satisfies:

, of occurring

conditional on occurring

(more simply the probability of given )

satisfies:

A singly conditional probability (i.e. order 1) is

e.g.  . A doubly

conditional probability (i.e. order 2) is e.g.

. A doubly

conditional probability (i.e. order 2) is e.g.  ,

probability of

,

probability of  occurring

given both and

occurring

given both and  take

specific values. Nil-conditioned conditional probabilities (i.e. order

0) are the marginal probabilities, e.g.

take

specific values. Nil-conditioned conditional probabilities (i.e. order

0) are the marginal probabilities, e.g.  . A Bayesian

network (more simply Bayesian net) is a directed acyclical graph where each

node/vertex, say

. A Bayesian

network (more simply Bayesian net) is a directed acyclical graph where each

node/vertex, say  is

associated with a random variable, say (often

a two-valued, i.e. Boolean, random variable) and with a conditional probability

table. For nodes without a parent the table contains just the marginal

probabilities for the values that might

take. For nodes with parents it contains all conditional probabilities for the

values that might

take given that its parents take specified values.

is

associated with a random variable, say (often

a two-valued, i.e. Boolean, random variable) and with a conditional probability

table. For nodes without a parent the table contains just the marginal

probabilities for the values that might

take. For nodes with parents it contains all conditional probabilities for the

values that might

take given that its parents take specified values.

4.3 Compound distributions

If  are

independent identically distributed random variables with moment generating

function

are

independent identically distributed random variables with moment generating

function  and

and  is an

independent non-negative integer-valued random variable then

is an

independent non-negative integer-valued random variable then  (with

(with  when

when  ) has

the following properties:

) has

the following properties:

For example, the compound Poisson distribution has:  and

and  where

where  and

and

NAVIGATION LINKS

Contents | Prev | Next