Enterprise Risk Management Formula Book

Appendix A.1: Probability Distributions:

Discrete (univariate) distributions

[this page | pdf | back links]

A.1 Discrete (univariate) distributions:

Binomial (and Bernoulli), Poisson

|

Distribution name

|

Binomial

distribution

|

|

Common notation

|

|

|

Parameters

|

= number of

(independent) trials, positive integer = number of

(independent) trials, positive integer

= probability

of success in each trial, = probability

of success in each trial,

|

|

Support

|

|

|

Probability mass

function

|

|

|

Cumulative distribution

function

|

|

|

Mean

|

|

|

Variance

|

|

|

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Characteristic function

|

|

|

Other comments

|

Corresponds to the number of successes in a sequence of independent

experiments each of which has a probability of

being successful.

The Bernoulli distribution is  and

corresponds to the likelihood of success of a single experiment. Its

probability mass function and cumulative distribution function are: and

corresponds to the likelihood of success of a single experiment. Its

probability mass function and cumulative distribution function are:

The Bernoulli distribution with  , i.e. , i.e.  , has the

minimum possible excess kurtosis, i.e. , has the

minimum possible excess kurtosis, i.e.  . .

The mode of  is is  if if  is 0 or not

an integer and is if is 0 or not

an integer and is if  . If . If  then the

distribution is bi-modal, with modes and then the

distribution is bi-modal, with modes and  . .

|

|

Distribution name

|

Poisson distribution

|

|

Common notation

|

|

|

Parameters

|

= event rate

( = event rate

( ) )

|

|

Support

|

|

|

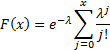

Probability mass

function

|

|

|

Cumulative distribution

function

|

(can also be expressed using the incomplete gamma

function)

|

|

Mean

|

|

|

Variance

|

|

|

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Characteristic function

|

|

|

Other comments

|

Expresses the probability of a given number of events

occurring in a fixed interval of time if the events occur with a known

average rate and independently of the time since the last event.

The median is approximately  . .

The mode is  if is

not integral. Otherwise the distribution is bi-modal with modes and if is

not integral. Otherwise the distribution is bi-modal with modes and

. .

|

NAVIGATION LINKS

Contents | Prev | Next