Enterprise Risk Management Formula Book

Appendix A.2: Probability Distributions:

Continuous (univariate) distributions (c) generalised Pareto, lognormal,

Student’s t

[this page | pdf]

Distribution name

Generalised

Pareto distribution (GPD)

|

|

Common notation

|

|

|

Parameters

|

= shape

parameter = shape

parameter

= location

parameter = location

parameter

= scale

parameter ( = scale

parameter ( ) )

|

|

Domain

|

|

|

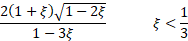

Probability density

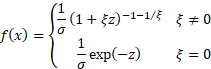

function

|

where

|

|

Cumulative distribution

function

|

|

|

Mean

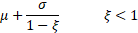

|

|

|

Variance

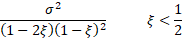

|

|

|

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Other comments

|

GPD is used in the peaks over thresholds variant of

extreme value theory

|

|

Distribution name

|

Lognormal

distribution

|

|

Common notation

|

|

|

Parameters

|

= scale

parameter ()

= location

parameter

|

|

Domain

|

|

|

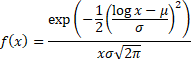

Probability density

function

|

|

|

Cumulative distribution

function

|

|

|

Mean

|

|

|

Variance

|

|

|

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Characteristic function

|

No simple expression that is not divergent

|

|

Other comments

|

The median of a lognormal distribution is  and its

mode is and its

mode is  . .

The truncated moments of  are: are:

|

|

Distribution name

|

(Standard)

Student’s t distribution

|

|

Common notation

|

|

|

Parameters

|

= degrees

of freedom ( = degrees

of freedom ( , usually is

an integer although in some situations a non-integral can

arise) , usually is

an integer although in some situations a non-integral can

arise)

|

|

Domain

|

|

|

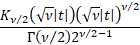

Probability density

function

|

|

|

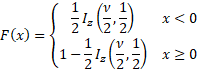

Cumulative distribution

function

|

where

|

|

Mean

|

|

|

Variance

|

|

|

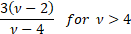

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Characteristic function

|

where  is a

Bessel function is a

Bessel function

|

|

Other comments

|

The Student’s t distribution (more simply the t

distribution) arises when estimating the mean of a normally distributed

population when sample sizes are small and the population standard deviation

is unknown.

It is a special case of the generalised hyperbolic

distribution.

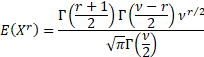

Its non-central moments if  is

even and is

even and  are: are:

If is even

and  then then  , if is

odd and then , if is

odd and then  and if is

odd and then and if is

odd and then  is undefined. is undefined.

|

NAVIGATION LINKS

Contents | Prev | Next