Deriving the Black-Scholes Option Pricing

Formulae using Ito (stochastic) calculus and partial differential equations

[this page | pdf | references | back links]

The following partial differential equation is satisfied by

the price of any derivative on  , given the assumptions

underlying the Black-Scholes world:

, given the assumptions

underlying the Black-Scholes world:

This partial differential equation is a second-order, linear

partial differential equation of the parabolic type. This type of

equation is the same as used by physicists to describe diffusion of heat. For

this reason, Gauss-Weiner or Brownian processes are also often commonly called diffusion

processes.

If  ,

,  and

and  are

constant then we can solve it by transforming it into a standard form which

others have previously solved, namely (for some constant

are

constant then we can solve it by transforming it into a standard form which

others have previously solved, namely (for some constant  ):

):

This can be achieved by replacing  by

by  where

where

(as long as is

constant) and by making the following double transformation (assuming that , and are

constant):

(as long as is

constant) and by making the following double transformation (assuming that , and are

constant):

This transformation removes one of the terms in the partial

differential equation:

The partial differential equation then simplifies to  , with

, with  . Prices of different

derivatives all satisfy this equation and are differentiated by the imposition

of different boundary conditions. A common tool for solving partial

differential equations subject to such boundary conditions is the use of Green’s

functions. This expresses the solution to a partial differential equation

given a general boundary condition applicable at some boundary

. Prices of different

derivatives all satisfy this equation and are differentiated by the imposition

of different boundary conditions. A common tool for solving partial

differential equations subject to such boundary conditions is the use of Green’s

functions. This expresses the solution to a partial differential equation

given a general boundary condition applicable at some boundary  , formed say by the

curve

, formed say by the

curve  , as an expression of

the following form, in which

, as an expression of

the following form, in which  is called the Green’s

function for that partial differential equation:

is called the Green’s

function for that partial differential equation:

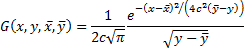

The Green’s function for where is

constant is:

If the boundary condition is expressed as  at

at  , where

, where  is continuous and

bounded for all

is continuous and

bounded for all  , then the solution is:

, then the solution is:

For a European call option, with strike price  , we

have, after making the substitutions described above,

, we

have, after making the substitutions described above,  . After some further

substitutions we find that this implies that:

. After some further

substitutions we find that this implies that:

where:

Substituting  and

and  into the formula for

into the formula for  recovers the

Black-Scholes formulae, e.g. for a call option:

recovers the

Black-Scholes formulae, e.g. for a call option:

Where

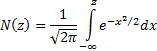

and  is the cumulative

Normal distribution function, i.e.

is the cumulative

Normal distribution function, i.e.